-

Timeline Mapping: From Lease to Ownership

Moving from renting to owning a home is a major step. It is not only about signing papers but also about planning each stage carefully. A clear timeline helps renters understand what to expect and how to prepare for ownership. Starting with the Lease Most journeys begin with a lease. Renters often choose a lease

-

Buyer Triggers: Signs You’re Ready to Transition from Renting

For many renters, the idea of owning a home feels distant. Rising costs, strict lending rules, and the comfort of short leases often keep people in apartments longer than they planned. Yet there comes a point when renting no longer fits your lifestyle or financial goals. Recognizing the signs that you are ready to move

-

Rent-to-Own vs Owner Financing: Which One Fits Your Situation

Rent-to-own and owner financing both offer alternative paths to homeownership. They appeal to buyers who may not qualify for traditional mortgages or who want more flexibility. But these two options work in very different ways. Choosing the right one depends on your financial situation, long-term goals, and how ready you are to take on ownership

-

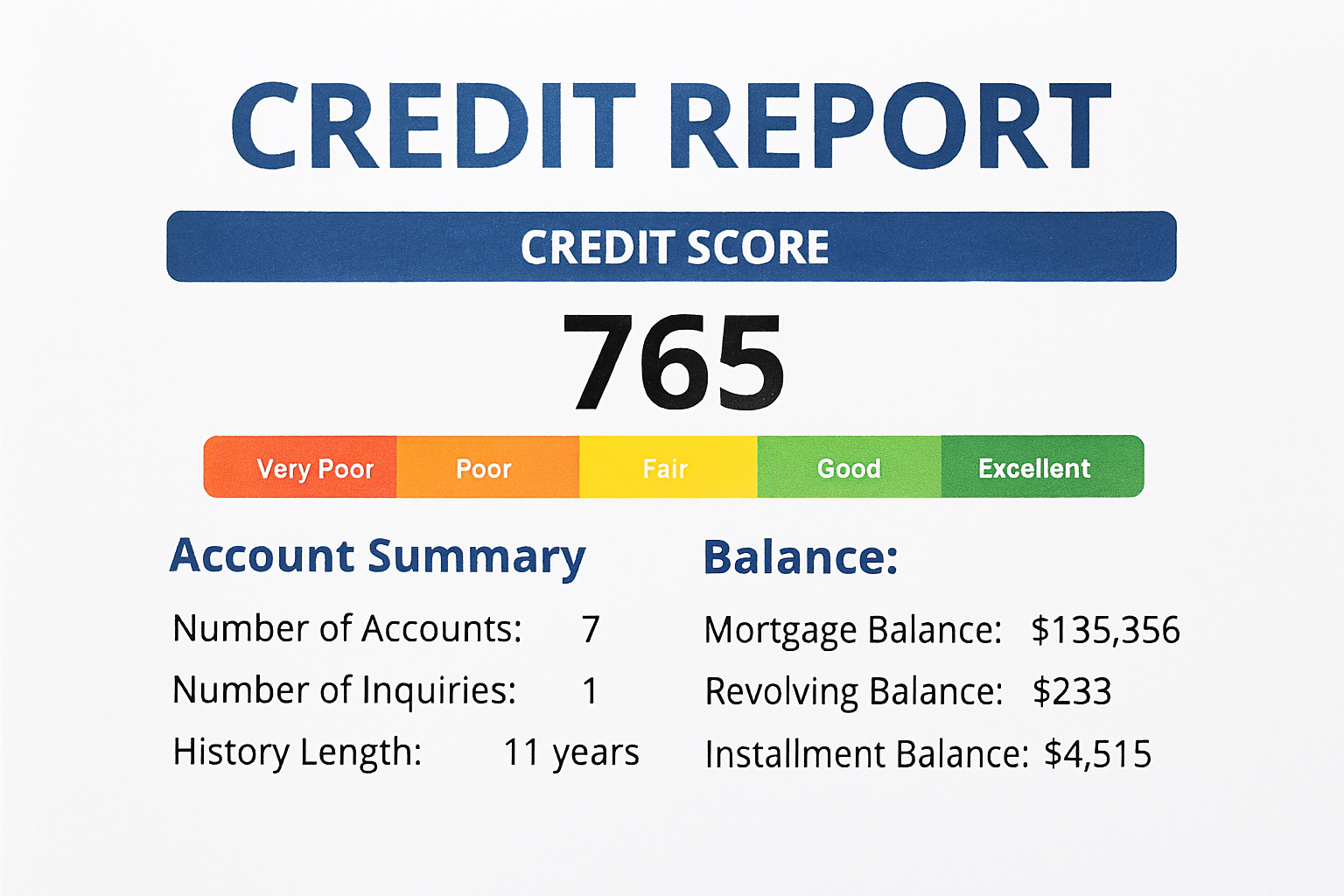

How Rent-to-Own Impacts Your Credit Over Time

Rent-to-own agreements offer a flexible path to homeownership, especially for buyers who need time to improve their credit. While these deals do not always show up on your credit report, they can still affect your credit in indirect ways. Understanding how rent-to-own impacts your credit over time helps you avoid setbacks and prepare for loan

-

How to Save for a Down Payment While Renting-to-Own

Rent-to-own agreements give buyers a chance to live in the home they plan to purchase while preparing financially. One of the biggest hurdles in that process is saving for a down payment. Even if part of your rent goes toward the purchase price, you will likely need extra cash at closing. That means building a

-

Credit Score Requirements for Rent-to-Own Buyers

Rent-to-own agreements offer a flexible path to homeownership, especially for buyers who need time to improve their credit. These deals let you rent a home now and buy it later, often with a portion of your rent going toward the purchase. But while credit checks may be relaxed at the start, your credit score still

-

Rent-to-Own and Debt: What You Need to Know

Rent-to-own housing may look like a shortcut to homeownership. You move in, pay monthly rent, and eventually buy the place. But behind the promise of ownership lies a web of financial risks that many buyers overlook. These deals often blur the line between renting and buying, and that confusion can lead to debt traps. Here

-

Can You Use FHA Loans for Rent-to-Own Properties

Rent-to-own agreements may seem like a flexible path to homeownership, especially for buyers with limited savings or credit challenges. These arrangements allow tenants to lease a home with the option to buy it later, often applying a portion of rent toward the purchase price. But when it comes to using an FHA loan to complete

-

How to Use Rent Credits Toward Your Purchase Price

Rent-to-own agreements offer a flexible path to homeownership, especially for buyers who need time to build credit, save for a down payment, or stabilize their income. One of the most valuable features in these agreements is the rent credit. This is a portion of your monthly rent that can be applied toward the future purchase

-

How to Budget for Rent-to-Own Monthly Payments

Rent-to-own agreements offer a flexible way to move toward homeownership, especially for buyers who need time to build credit or save for a mortgage. But flexibility does not mean low cost. These deals come with unique financial responsibilities that require careful planning. Budgeting for monthly payments is one of the most important steps in making